")

Tokens Playing This P2E Game")

Blockchain technology has come a long way. Starting from mere promises, it now powers a handful of significant projects. Thus, a number of public bodies, enterprises, and organizations around the world are adopting it at a steady pace. In India, the story is no different.

In 2018, India’s Reserve Bank banned cryptocurrency-related transactions through banks. Though the ban is still there, the blockchain working space seems to be expanding. Let’s take a closer look.

India’s steps towards blockchain adoption

- The government

Many state governments have initiated different blockchain projects that will help address different social needs. Currently, most of these projects are in the pilot stage. Yet, state governments are showing a progressive approach in welcoming start-ups and providing them with a suitable environment to participate in these initiatives.

That said, the private enterprises across all key industries in India are also identifying different applications of blockchain. The Banking, Financial Services and Insurance (BFSI) sector is the leading adopter of the new technology. However, other industries, including healthcare, retail, and logistics are not lagging behind.

- Blockchain congress

NITI Aayog, the Indian government’s subsidiary, hosted the International Blockchain Congress in 2018 along with the state governments of Telangana and Goa. The idea was to promote blockchain adoption in the country and to outline the present scenario.

- Research

In 2018, the Reserve Bank of India set up a group of blockchain app development researchers. Their goal is to create a cashless and decentralized banking system.

- Blockchain patents

India ranks 6th in the world for blockchain patent approvals. The footprint is therefore strong.

- Developers’ presence

According to a report by Dappros, a London-based consulting firm, India has the second-largest number of blockchain developers — 19,627 — in the world, following the United States.

- The Finance Minister’s take

In February 2019, the Finance Minister, Arun Jaitley, stated that the government was exploring the use of the blockchain for promoting the digital economy.

At the same time, the NITI Aayog is considering using blockchain technology for the fertilizer and drug industries.

Many Indian states, including Karnataka, Telangana, Kerala, and Maharashtra, are willing to use blockchain for the voting procedure. Ultimately, making it transparent and secure.

India’s challenges in adopting blockchain tech

As technology continues to reshape industries, the future of blockchain looks bright. However, there are also certain challenges ahead:

-

Lack of regulation

Lack of regulation regarding cryptocurrencies has resulted in ubiquitous uncertainty. As a result, blockchain start-ups aren’t fully sure how to operate.

-

Sour taste from the past

The decision by the Reserve Bank of India to prohibit banks from carrying out crypto transactions has created confusion. Many thought that this meant that crypto is completely banned in India. Consequently, regular Indian investors hesitated to invest in blockchain startups.

-

Lack of people

New technologies require specific skills. Most of India’s IT Companies are currently offering blockchain services and hence there is a huge demand for individuals with know-how.

Yet, there are simply not enough people. Besides, at universities, the courses are limited. As a result, blockchain companies are trying to fill the gap by giving cross-domain training to the existing employees.

-

Cost

For public-based blockchain apps, the cost of network maintenance and validation of transactions is high.

-

Adoption of new technology

Since blockchain technology is still in the research phase, many people are not aware of it.

-

Insufficient investments

The investments in the Indian blockchain system are comparatively low. Accordingly, they stand at less than 0.2% of all the global investments. In total, blockchain companies have managed to secure a total of $8.5 million through VC firms and ICOs.

Due to the regulatory and legal risk around blockchain in India, global investors are finding it difficult to invest in Indian start-ups, even though they develop innovative solutions. Some of the crypto exchanges such as Unocoin and Zebpay were forced to pack up.

Consequently, several India-based investors are raising funds through VCs and ICOs in other jurisdictions such as Malta, Singapore, UK, Switzerland, etc. that have a favorable regulatory environment.

India’s public sector is emerging as the largest consumer of blockchain technology

The government is playing an important role not only as a regulator but also as a consumer of blockchain solutions in India. Currently, 40+ Blockchain initiatives are being executed by the public sector in India, with ~92% in the pilot/POC phase and ~8% projects in the production phase.

- The government of Telangana and the government of Andhra Pradesh are two of the leading states in terms of blockchain adoption in India. Other state governments are also showing interest in this technology;

- Since a majority of the blockchain pilot programs were initiated in 2018, the benefits of these projects will likely materialize in the 2020s;

- Most of the initiated pilot programs focus on the land registry, governmental administrative work, compliance and security measures;

- Compared to 2017, the number of projects in the POC phase increased by seven times while projects in the pilot phase — by 6 times.

Areas where blockchain research and innovation are under development

- Eliminating counterfeit drugs

- Farm insurance

- Identity management

- Power distribution

- Duty payments

- Vehicle lifecycle management

- Organ tracking for transplants

- Rationing

- e-Governance

- Chit fund operations administration

- Microfinance for Self-Help Groups (SHG)

- Cybersecurity

- Agriculture supply chain

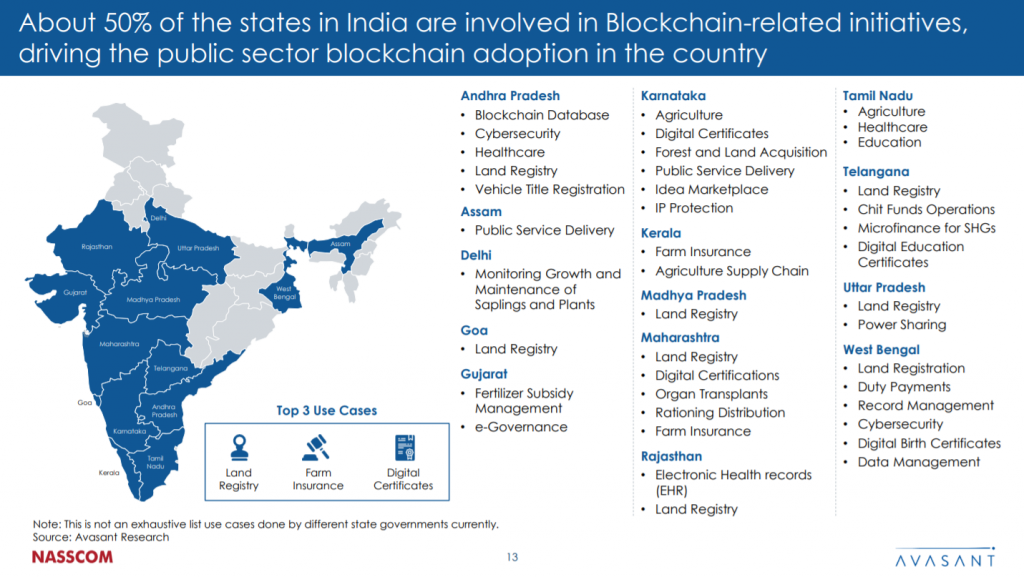

More than half of the Indian state governments have adopted blockchain for various projects

Below is a detailed report from NASSCOM. It shows the industries chosen by different states.

Source: NASSCOM Avasant India Blockchain Report 2019

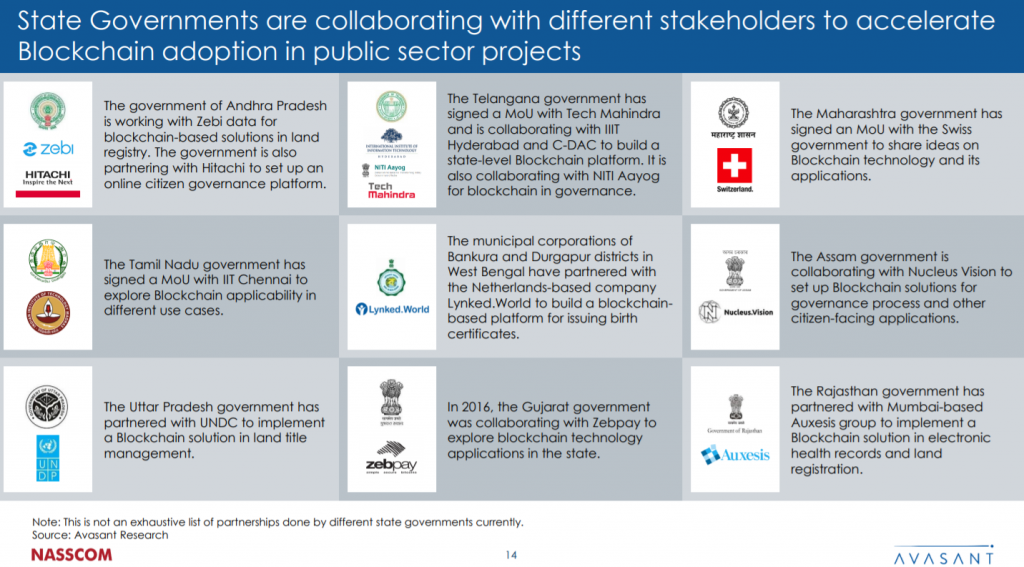

State government are collaborating with different stakeholders to accelerate blockchain adoption in India

Source: NASSCOM Avasant India Blockchain Report 2019

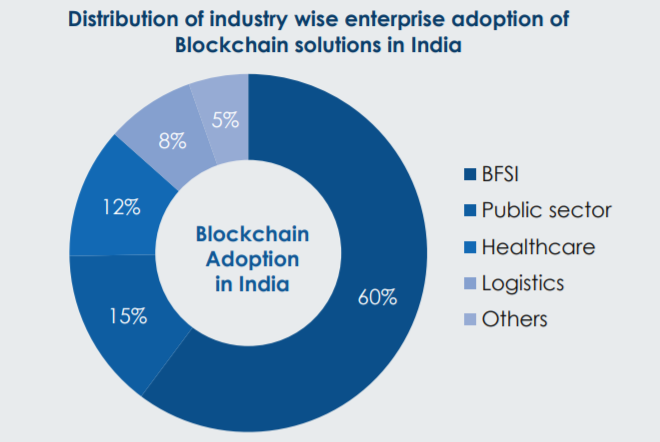

Industry-wise distribution of blockchain adoption in India

In India, the BFSI is adopting blockchain at the fastest pace. Healthcare, retail, and manufacturing sectors are also in the game.

Source: NASSCOM Avasant India Blockchain Report 2019

Conclusion

There is no doubt that blockchain has caught the world’s attention. To that end, India is also trying to streamline its fast-growing economy to fully explore blockchain’s potential.

Currently, there are decent Indian projects like Matic and Zebi. It’s worth remembering that the Indian market is big, and the recent Wazirx acquisition by Binance proves it.

All in all, India needs to step up its blockchain game. And give the new technology a chance to shine.

References

NASSCOM Avasant India Blockchain Report 2019

Join us on Telegram to receive free trading signals.

For more cryptocurrency news, check out the Altcoin Buzz YouTube channel.

Staking 2.0 Launches With More Rewards")

{kind=link}

This blog is full of knowledge & boost up my inner capability towards blockchain adoption.