A new market surfaces in DeFi, undercollateralized and uncollateralized loans.

This is a fairly new niche in DeFi. However, a few lending protocols offer this now. Time to dig in and see what’s cooking in DeFi yield.

Undercollateralized (UC) and uncollateralized lending (UCL) protocols. These are the new kids on the DeFi lending block. Typically, DeFi uses overcollateralized lending. In the following twitter thread from Spencernoon.eth, you will see more about this crypto lending services:

Note: Spencernoon.eth is an active Crypto Twitter person, dove deep into this with a thread, dedicated to this topic. He is a respected investor and General Partner at Variant.fund. Furthermore, he is also part of a free weekly newsletter for on-chain alpha leaks. That is Ournetwork.

It’s important to let you know that the DeFi lending market is to reach $1 trillion in value, according to a Polygontech blog. DeFi will reach this milestone with two approaches.

However, UC (undercollateralized lending) is causing restrictions. As a result, DeFi adoption is in the waiting room.

Source: Polygon tech blog

We will look more in-depth at four new protocols. Their biggest issue to solve is identity and reputation from a borrower. How can they lend UC or UCL to an anon Twitter person and knowing they still get their loan back? That’s not an easy task when dealing with on-chain logistics. One possible solution is to complete KYC off-chain.

An interesting add-on is that we also see some PMF (Product-Market Fit). PMF is a very important marketing strategy. In a nutshell, it means that a new product enters the market as a dress rehearsal. As a result, this will show how well the market accepts it.

So, let’s have a look at four protocols that offer UC and UCL loans. How they do it and to whom.

Compared to other protocols, their outstanding loans are not that big. However, it’s a start, and they all offer UC or UCL loans. That does make them stand out.

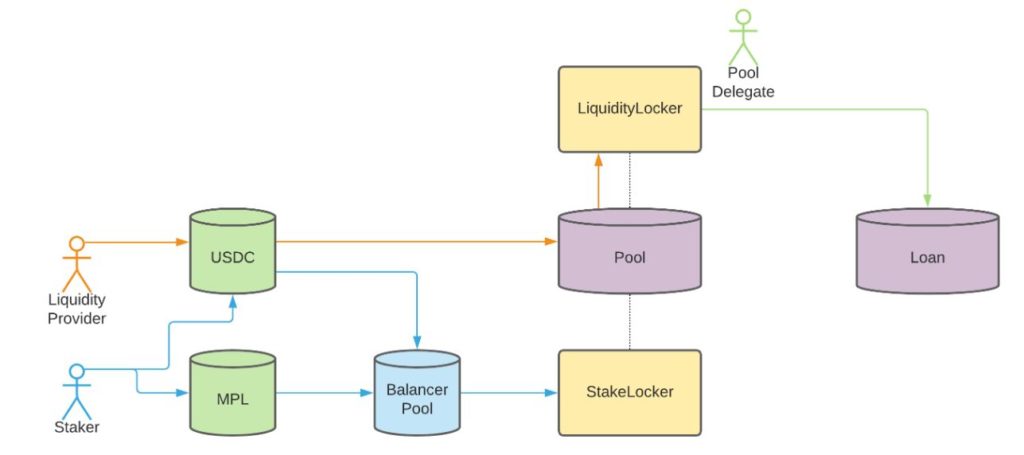

The picture below shows how Maple works.

Source: Maple Github

Moreover, now, the first three, Maple, TrueFi and Clearpool have something in common. They all lend to credible crypto institutions like.

The reason being? The UCL they offer has better DeFi yield rates than what they get outside of crypto!

There is also a reason why they offer these loans only to institutions and not to retailers. That reason is fairly simple. Currently, they don’t have the means to KYC thousands of retailers. This KYC happens off-chain. For example, Teller offers such a service.

Goldfinch approaches this with a different angle. Moreover, they lend to institutions in emerging markets. For example, they collateralize their loans differently. In addition, they use off-chain assets. Currently, they offer some of the most attractive DeFi yields. How about 10% to 34% DeFi yield and the GFI token is the reward?

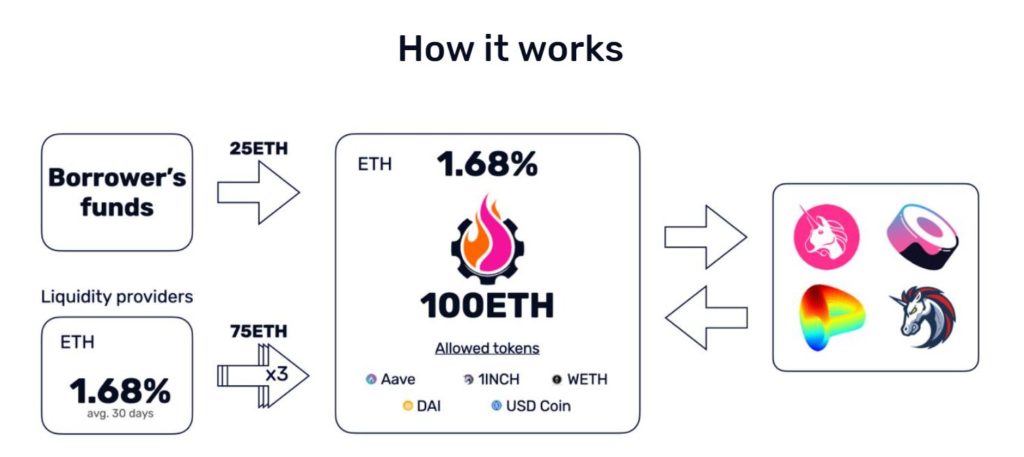

A protocol that caters to retail is Gearbox Protocol. They boast a TVL of $17 million. Whitelisted protocols, like Uniswap, Curve, or Yearn, have 10x leverage. Also, they roll their product out slowly, but it should be available for testing very soon.

Source: Gearbox Protocol

In addition, some protocols cover their LPs with a form of insurance. They do this, for instance, by diverting a percentage of each pool’s interest to an insurance pool. This shows that they are working on ways to cover their LPs from forfeited loans.

On the other hand, we see many innovative ways to offer UC and UCL loans. Each protocol has a different way how they want to solve this riddle. Most importantly, DeFi lending changes with these protocols. Small loans, student loans, or mortgages can turn in the future to these protocols.

Moreover, there are still issues that they need to iron out. For example, scalability, regulation, or relying on off-chain KYC. However, they made a start, which is important.

⬆️Finally, for more cryptocurrency news, check out the Altcoin Buzz YouTube channel.

⬆️Above all, find the most undervalued gems, up-to-date research, and NFT buys with Altcoin Buzz Access. Join us for $99 per month now.

Casper Network is betting big on EVM support, AI payments, and quantum-safe blockchain infrastructure with its new multi-year roadmap.

Microsoft's bet on Space and Time is starting to pay off with the launch of Dreamspace, a no code app builder

Worldcoin's World ID is now live and updated. It's out to prove you are human when on the web instead of dealing with a bot.

Stable yields on top lending protocols are down to less than 2%...but 10%+ #DeFi yields are far from dead. Here's where the yield party went 👇🧵